Changes to the Australian Superannuation Payments as of July 2026: What Female Small Business Owners Need to Know

Disclaimer: This blog post is intended for informational purposes only and does not constitute legal, financial, visa, or medical advice. Please consult with a qualified professional for advice tailored to your specific situation.

From July 2026, Australian superannuation rules are undergoing their biggest shake-up in years. The move to payday super, new contribution caps, government-paid super on parental leave, and digital upgrades will impact every small business owner. Understanding these changes is essential for compliance, cash flow, and supporting your team—especially for women in business.

Why Superannuation Changes Matter for Women in Business

As the owner of an online business management consultancy dedicated to empowering female small business owners across Australia, I know how crucial it is to stay ahead of regulatory changes. Superannuation is not just a compliance box to tick—it’s a cornerstone of financial security for you and your team, especially for women who often face unique retirement savings challenges.

With sweeping reforms coming into effect from July 2026, now is the time to get informed, get prepared, and turn these changes into opportunities for your business and your people.

Table of Contents

The Payday Super Revolution: From Quarterly to Payday Payments

Super Guarantee Rate: Locked in at 12%

Super on Paid Parental Leave: A Win for Women’s Retirement

Contribution Caps: More Room to Grow Your Super

SuperStream Version 3 and STP Reporting: The Digital Upgrade

Transfer Balance Cap: Indexing to $2.1 Million

ATO Compliance Approach: The First Year of Payday Super

Practical Action Steps for Small Business Owners

Conclusion: Embracing Change, Empowering Women

Disclaimer

The Payday Super Revolution: From Quarterly to Payday Payments

What’s Changing?

From 1 July 2026, employers must pay superannuation contributions for their employees on payday, not monthly or quarterly. This is a seismic shift from the old system, where super could be paid only four times a year. Now, every time you pay your staff, you must also pay their super—ensuring their retirement savings grow in real time.

Key Details

Deadline: Super contributions must reach the employee’s super fund within 7 business days after each payday.

No more Small Business Superannuation Clearing House (SBSCH): The SBSCH will close permanently from 1 July 2026. You’ll need to use a commercial clearing house or SuperStream-compliant payroll software.

Why This Matters

Cash Flow: You’ll need to manage cash flow more closely, as super payments will be more frequent.

Compliance: Missing the 7-day deadline triggers the Superannuation Guarantee Charge (SGC), which is not tax-deductible and comes with hefty penalties.

Employee Benefits: Employees’ super grows faster, with less risk of missed or late payments.

Key Finding:

The move to payday super is designed to close the $3.6 billion annual gap in unpaid super and boost retirement savings, especially for women who are more likely to experience interrupted work patterns.

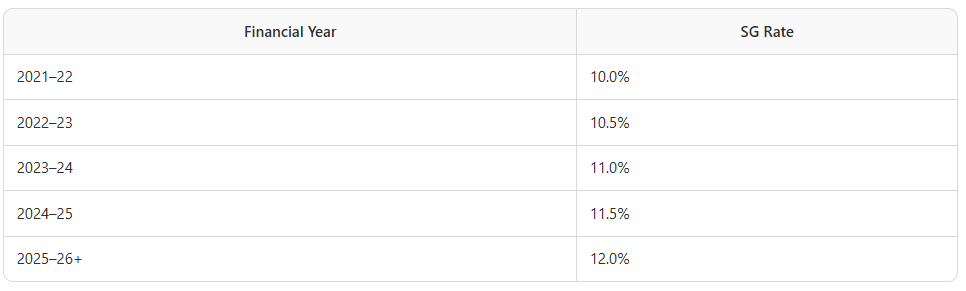

Super Guarantee Rate: Locked in at 12%

The Final Step in a Decade-Long Increase

The Superannuation Guarantee (SG) rate—the percentage of ordinary time earnings that must be paid into super—reached its legislated maximum of 12% from 1 July 2025 and remains at this rate from July 2026 onwards.

SG Rate Schedule

No further increases are scheduled.

Employers must apply the 12% rate to all eligible employees’ ordinary time earnings.

What This Means for You

Budgeting: Factor the 12% rate into your payroll and cash flow planning.

Payroll Systems: Ensure your payroll software is updated to calculate super at 12%.

No More Guesswork: The rate is now stable, making long-term planning easier.

Super on Paid Parental Leave: A Win for Women’s Retirement

The Game-Changer for Gender Equity

From July 2026, the Australian Government will pay superannuation on government-funded Paid Parental Leave (PPL) for children born or adopted from 1 July 2025. This is a landmark reform for women’s retirement savings.

How It Works

Who Pays? The government (via the ATO), not the employer.

How Much? 12% of the total Parental Leave Pay received.

When? Paid as a lump sum into the employee’s super fund after the end of the financial year in which PPL was received.

Eligibility: Applies to all eligible parents (including self-employed) who receive government-funded PPL for a child born/adopted from 1 July 2025.

Example Calculation

If an employee receives the full 24 weeks of Parental Leave Pay at $948.10 per week (2025–26 rate):

Total PPL: 24 x $948.10 = $22,754.40

Super Contribution: 12% x $22,754.40 = $2,730.53 (paid by the ATO)

What Employers Need to Do

Nothing extra: No calculation, payment, or reporting required for this super. The ATO handles it all.

Continue normal obligations: If you offer employer-funded paid parental leave, you must still pay super on that leave as per existing rules.

Why This Matters for Women

Bridges the super gap: Women are more likely to take parental leave and have lower super balances at retirement. This reform helps close that gap.

No cost or admin burden: Small business owners can support their team’s financial future without extra paperwork or expense.

Key Takeaway:

Super on government-funded PPL is a major win for women’s retirement security—delivered with zero extra admin for small business owners.

Have you checked out all the new tools, guides and checklists in our Resource Hub? Explore and download now!

Contribution Caps: More Room to Grow Your Super

Higher Limits for 2026–27

From 1 July 2026, the annual caps on how much can be contributed to super will increase, giving business owners and employees more flexibility to boost retirement savings.

New Caps

Concessional contributions include employer SG, salary sacrifice, and personal deductible contributions.

Non-concessional contributions are after-tax contributions.

Bring-forward rule: Eligible individuals can contribute up to three years’ worth of non-concessional caps in one go, subject to their total super balance.

Maximum Super Contribution Base

For 2026–27, employers are not required to pay SG on earnings above $250,000 per employee per year.

Transfer Balance Cap

The general transfer balance cap (the maximum you can transfer into a tax-free retirement pension) increases to $2.1 million from 1 July 2026.

Why This Matters

More flexibility: Higher caps allow for catch-up contributions, especially useful for women returning to work after career breaks.

Tax planning: Consider salary sacrifice or personal contributions to maximize tax benefits and retirement savings.

SuperStream Version 3 and STP Reporting: The Digital Upgrade

SuperStream Version 3

SuperStream is the standard for electronic super payments and data. From 1 July 2026, SuperStream Version 3 brings:

Faster payments: Near real-time processing via the New Payments Platform (NPP).

Clearer error messages: Easier to fix rejected contributions.

Member Verification Request (MVR): Payroll software can verify employee super fund details before payment, reducing errors.

Funds must allocate or return contributions within 3 business days (down from 20).

Single Touch Payroll (STP) Phase 2

From 1 July 2026, employers must report both qualifying earnings (QE) and super liability through STP.

STP reporting remains compulsory for all employers.

SBSCH Closure

The Small Business Superannuation Clearing House (SBSCH) closes permanently from 1 July 2026.

Transition to a commercial clearing house or SuperStream-compliant payroll software before this date.

Why This Matters

Efficiency: Faster, more accurate super payments.

Compliance: Automated reporting reduces risk of errors and penalties.

Preparation: Review your payroll systems and processes now to ensure they’re ready for the new standards.

Transfer Balance Cap: Indexing to $2.1 Million

The transfer balance cap is the maximum amount you can transfer into a tax-free retirement pension account. From 1 July 2026, this cap increases to $2.1 million.

Impacts: Non-concessional contribution eligibility, tax-free pension phase, and estate planning.

Planning tip: If you’re approaching retirement, review your super strategy with a financial adviser to make the most of the new cap.

ATO Compliance Approach: The First Year of Payday Super

A Practical, Supportive Transition

The ATO has announced a practical compliance approach for the first year of payday super (2026–27):

Focus on education: The ATO will prioritize helping employers understand and implement the new rules.

Genuine effort matters: Employers making genuine efforts to comply and resolve errors quickly are less likely to face penalties.

No leniency for deliberate non-compliance: Those who ignore the new rules or fail to fix issues may face audits and penalties.

Penalties for Non-Compliance

Super Guarantee Charge (SGC): Includes unpaid super, 10% interest, and a $20 admin fee per employee per quarter.

Additional penalties: Up to 200% of the SGC for serious breaches.

SGC is not tax-deductible.

Key Finding:

Early preparation and proactive communication with your payroll provider or bookkeeper will make the transition to payday super smooth and stress-free.

Practical Action Steps for Small Business Owners

1. Review and Update Payroll Systems

Check compatibility: Ensure your payroll software can process super payments on payday and is SuperStream Version 3 compliant.

Automate payments: Set up automated super payments to avoid missing the 7-day deadline.

2. Plan for Cash Flow Changes

Forecast cash flow: More frequent super payments mean you’ll need to manage cash flow more closely.

Adjust payment cycles: Consider aligning pay cycles with your business’s cash flow patterns.

3. Transition from SBSCH

Choose a new clearing house: Research commercial clearing houses or upgrade your payroll software before 1 July 2026.

Test the new system: Run a trial to ensure payments and reporting work smoothly.

4. Communicate with Your Team

Inform employees: Let your staff know about the changes, especially the benefits of more frequent super payments and super on parental leave.

Support working parents: Highlight the new government-paid super on PPL as a positive step for women’s financial security.

5. Maximize Super Contributions

Review contribution caps: Consider salary sacrifice or personal contributions to take advantage of higher caps.

Catch-up contributions: If your super balance is under $500,000, you may be able to carry forward unused concessional caps from previous years.

6. Stay Informed and Seek Advice

Monitor updates: Keep an eye on ATO and government announcements for any further changes.

Consult professionals: Work with your accountant or financial adviser to ensure compliance and optimize your super strategy.

Conclusion: Embracing Change, Empowering Women

The July 2026 superannuation reforms are more than just regulatory tweaks—they’re a chance to build a stronger, fairer future for women in business. By embracing payday super, supporting parental leave super, and leveraging higher contribution caps, you can empower yourself and your team for long-term financial security.

Change can be daunting, but with the right knowledge and preparation, it’s also an opportunity. As female business owners, we have the power to lead by example—championing compliance, supporting our staff, and building businesses that thrive.

Let’s turn these superannuation changes into a win for our businesses, our employees, and our own financial futures.

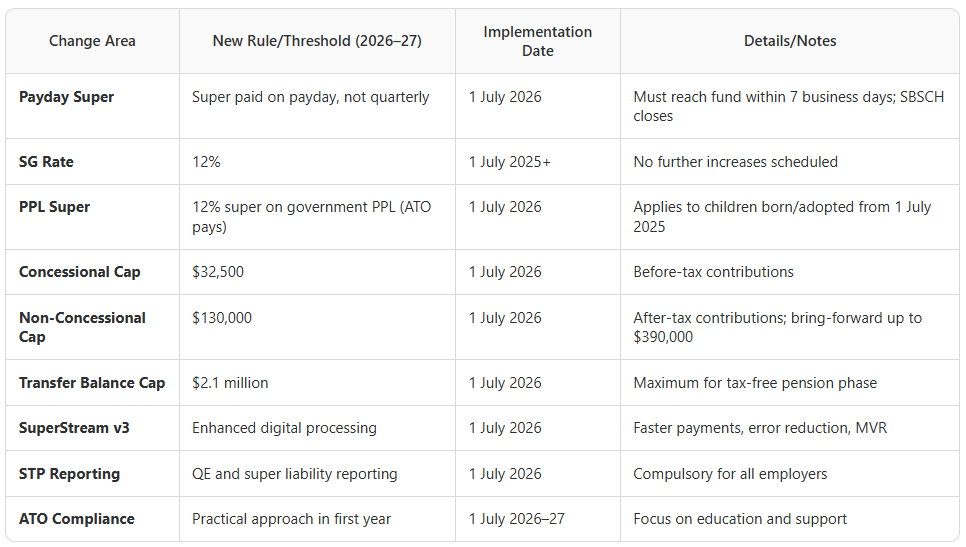

Quick Reference: July 2026 Superannuation Changes at a Glance

Disclaimer

This blog post is for general information only and does not constitute financial or tax advice. Every business is unique. Please consult a qualified accountant, tax adviser, or superannuation specialist to discuss your specific circumstances and ensure compliance with all relevant laws and regulations.

Want more inspiration and practical support? Subscribe to our newsletter for monthly insights, or book a one-on-one session to map outy the world!

There are many ways of working with professionals. Start small, but keep it regularly and don’t wait until something happens. Strategic planning and periodic reviews are a great start to implement those strategies.

Perfectly Organised NT can assist with a financial review and strategic business planning & management. Find out more!

Perfectly Organised NT - helping small business owners in Australia manage their business.